5 Simple Techniques For How Much Does A Having A Cosigner Help On Mortgages

Like other types of home loans, there are various types of reverse home mortgages. While they all essentially work the same method, there are three primary ones to understand about: The most common reverse home mortgage is the Home Equity Conversion Home Loan (HECM). HECMs were created in 1988 to assist older Americans make ends satisfy by enabling them to take advantage of the equity of their houses without needing to vacate.

Some folks will utilize it to pay for expenses, trips, house restorations or even to pay off the remaining quantity on their regular mortgagewhich is nuts! And the consequences can be huge. HECM loans are continued a tight leash by the Federal Housing Administration (FHA.) They do not want you to default on your mortgage, so because of that, you won't receive a reverse mortgage if your house is worth more than a specific quantity.1 And if you do receive an HECM, you'll pay a substantial home mortgage insurance premium that safeguards the here lender (not you) against any losses.

They're offered up from independently owned or operated business. And due to the fact that they're not controlled or guaranteed by the government, they can draw property owners in with promises of higher loan amountsbut with the catch of much greater rates of interest than those federally guaranteed reverse mortgages. They'll even provide reverse home mortgages that enable house owners to borrow more of their equity or include houses that surpass the federal maximum amount.

A single-purpose reverse home loan is provided by government firms at the state and local level, and by not-for-profit groups too. It's a type of reverse home loan that puts guidelines and limitations on how you can utilize the cash from the loan. (So you can't spend it on an elegant trip!) Generally, single-purpose reverse home loans can only be used to make real estate tax payments or pay for house repairs.

What Does What Are The Types Of Reverse Mortgages Mean?

The important things to keep in mind is that the loan provider has to approve how the cash will be used prior to the loan is given the OK. These loans aren't federally insured either, so loan providers don't need to charge home mortgage insurance coverage premiums (who took over abn amro mortgages). But considering that the cash from a single-purpose reverse mortgage needs to be used in a particular method, they're typically much smaller in their amount than HECM loans or exclusive reverse home mortgages.

Own a paid-off (or a minimum of significantly paid-down) house. Have this home as your main residence. Owe absolutely no federal debts. Have the capital to continue paying property taxes, HOA fees, insurance, upkeep and other house costs. And it's not just you that needs to qualifyyour home also has to meet particular requirements.

The HECM program likewise enables reverse home mortgages on condominiums approved by the Department of Real Estate and Urban Advancement. Before you go and sign the papers on a reverse home loan, take a look at these 4 significant drawbacks: You might be believing about getting a reverse home loan since you feel great borrowing versus your home.

Let's simplify like this: Envision having $100 in the bank, but when you go to withdraw that $100 in money, the bank just offers you $60and they charge you interest on that $60 from the $40 they keep. If you would not take that "deal" from the bank, why on earth would you desire to do it with your home you've spent decades paying a home loan on? However that's exactly what a reverse home mortgage does.

3 Simple Techniques For How Much Is Mortgage Tax In Nyc For Mortgages Over 500000:oo

Why? Because there are charges to pay, which leads us to our next point. Reverse https://writeablog.net/aspaido3ib/a-married-couple-filing-collectively-can-present-as-much-as-30-000-devoid-of home mortgages are packed with extra expenses. And most customers decide to pay these costs with the loan they're about to getinstead of paying them expense. The thing is, this expenses you more in the long run! Lenders can charge up to 2% of a home's value in an paid up front.

5% mortgage insurance coverage premium. So on a $200,000 home, that's a $1,000 annual expense after you've paid $4,000 upfront naturally!$14 on a reverse mortgage resemble those for a routine home loan and consist of things like house appraisals, credit checks and processing fees. So before you know it, you've sucked out thousands from your reverse home loan prior to you even see the very first cent! And since a reverse home mortgage is just letting you tap into a portion the worth of your house anyway, what happens once you reach that limitation? The cash stops.

So the quantity of money you owe increases every year, on a monthly basis and every day till the loan is settled. The advertisers promoting reverse mortgages enjoy to spin the old line: "You will never ever owe more than your house is worth!" However that's not precisely true because of those high rate of interest.

Let's state you live up until you're 87 - when did subprime mortgages start in 2005. When you die, your estate owes $338,635 on your $200,000 home. So instead of having a paid-for home to pass on to your loved ones after you're gone, they'll be stuck with a $238,635 expense. Opportunities are they'll have to sell the house in order to settle the loan's balance with the bank if they can't pay for to pay it.

The Best Guide To What Metal Is Used To Pay Off Mortgages During A Reset

If you're investing more than 25% of your earnings on taxes, HOA charges, and household bills, that means you're home poor. Connect to among our Backed Regional Suppliers and they'll assist you navigate your choices. If a reverse home loan lender informs you, "You will not lose your house," they're not being straight with you.

Think about the factors you were considering getting a reverse mortgage in the first location: Your budget plan is too tight, you can't manage your everyday expenses, and you don't have anywhere else to turn for some additional cash. All of a sudden, you have actually drawn that last reverse home loan payment, and after that the next tax costs happens.

If you do not pay your taxes or your other expenses, for how long will it be before someone comes knocking with a residential or commercial property seizure notification to eliminate the most valuable thing you own? Not extremely long at all. And that's possibly the single most significant factor you ought to prevent these predatory financial items.

Water shut off without notification, a letter resolved to a deceased mom, a loan that never should have been approved. Even heirs who wish to settle reverse mortgages to keep a family house, and have the ways to do so, can find themselves stymied by an apparently limitless cycle of clashing messages that extend for many years.

Everything about How Is The Compounding Period On Most Mortgages Calculated

Reverse home loans permit property owners to obtain versus the equity in their houses and remain in place mortgage-free until they pass away, while providing their heirs the alternative of paying off the loan to keep the residential or commercial properties or sell them. That's not how it exercised for the people who connected to USA TODAY (which banks are best for poor credit mortgages).

USA TODAYThe roadblocks they faced different extensively from paperwork mistakes to messy titles however all of them had one thing in typical: a desire to keep the residential or commercial property in the family. "My great, fantastic grandfather owned this home (start in) 1909," stated Latoya Gatewood-Young, who has fought for 4 Website link years to purchase the family home in Maryland.

Fascination About How Common Are Principal Only Additional Payments Mortgages

Like other types of mortgages, there are different types of reverse mortgages. While they all generally work the exact same way, there are three main ones to learn about: The most typical reverse home loan is the Home Equity Conversion Mortgage (HECM). HECMs were developed in 1988 to assist older Americans make ends fulfill by allowing them to take advantage of the equity of their houses without having to leave.

Some folks will utilize it to spend for costs, trips, home renovations or perhaps to pay off the Website link remaining amount on their regular mortgagewhich is nuts! And the consequences can be substantial. HECM loans are continued a tight leash by the Federal Real Estate Administration (FHA.) They don't want you to default on your home loan, so https://writeablog.net/aspaido3ib/a-married-couple-filing-collectively-can-present-as-much-as-30-000-devoid-of since of that, you will not get approved for a reverse home mortgage if your house is worth more than a specific quantity.1 And if you do qualify for an HECM, you'll pay a significant home mortgage insurance coverage premium that secures the lender (not you) against any losses.

They're provided from independently owned or operated business. And since they're not managed or insured by the federal government, they can draw property owners in with promises of higher loan amountsbut with the catch of much higher rates of interest than those federally guaranteed reverse mortgages. They'll even use reverse home mortgages that permit property owners to borrow more of their equity or consist of houses that surpass the federal optimum amount.

A single-purpose reverse home mortgage is provided by federal government companies at the state and local level, and by nonprofit groups too. It's a kind of reverse mortgage that puts guidelines and limitations on how you can use the cash from the loan. (So you can't spend it on a fancy trip!) Usually, single-purpose reverse home loans can only be used to make home tax payments or pay for home repairs.

Fascination About What Is A Non Recourse State For Mortgages

The important things to keep in mind is that the lending institution needs to authorize how the cash will be used before the loan is provided the OK. These loans aren't federally insured either, so lending institutions do not have to charge mortgage insurance coverage premiums (how to rate shop for mortgages). However since the cash from a single-purpose reverse mortgage needs to be utilized in a particular way, they're generally much smaller sized in their amount than HECM loans or exclusive reverse mortgages.

Own a paid-off (or at least significantly paid-down) house. Have this home as your primary house. Owe zero federal debts. Have the cash flow to continue paying real estate tax, HOA costs, insurance coverage, maintenance and other house expenditures. And it's not simply you that has to qualifyyour home also has to fulfill particular requirements.

The HECM program also permits reverse home mortgages on condos approved by the Department of Housing and Urban Advancement. Before you go and sign the papers on a reverse home mortgage, examine out these four significant drawbacks: You might be considering taking out a reverse mortgage due to the fact that you feel positive borrowing against your home.

Let's break it down like this: Picture having $100 in the bank, however when you go to withdraw that $100 in money, the bank just gives you $60and they charge you interest on that $60 from the $40 they keep. If you would not take that "deal" from the bank, why on earth would you desire to do it with your house you've spent years paying a home loan on? But that's precisely what a reverse home mortgage does.

Getting My Blank Have Criminal Content When Hacking Regarding Mortgages To Work

Why? Because there are charges to pay, which leads us to our next point. Reverse mortgages are loaded with extra expenses. And a lot of borrowers opt to pay these costs with the loan they're about to getinstead of paying them out of pocket. The thing is, this costs you more in the long run! Lenders can charge up to 2% of a house's value in an paid up front.

5% home loan insurance coverage premium. So on a $200,000 home, that's a $1,000 yearly expense after you've paid $4,000 upfront obviously!$14 on a reverse home mortgage are like those for a routine home mortgage and consist of things like home appraisals, credit checks and processing costs. So prior to you understand it, you have actually sucked out thousands from your reverse mortgage before you even see the very first penny! And because a reverse home mortgage is only letting you tap into a portion the value of your house anyhow, what happens as soon as you reach that limit? The money stops.

So the amount of money you owe increases every year, on a monthly basis and every day till the loan is settled. The advertisers promoting reverse home mortgages like to spin the old line: "You will never ever owe more than your home deserves!" However that's not precisely true since of those high rates of interest.

Let's state you live until you're 87 - how many mortgages to apply for. When you pass away, your estate owes $338,635 on your $200,000 house. So rather of having a paid-for house to hand down to your liked ones after you're gone, they'll be stuck with a $238,635 costs. Possibilities are they'll need to offer the house in order to settle the loan's balance with the bank if they can't manage to pay it.

The What Is The Interest Rate Today On Mortgages Ideas

If you're spending more than 25% of your earnings on taxes, HOA costs, and family costs, that suggests you're house poor. Reach out to among our Backed Local Service Providers and they'll assist you browse your choices. If a reverse mortgage lending institution informs you, "You will not lose your house," they're not being straight with you.

Consider the reasons you were considering getting a reverse home mortgage in the first location: Your budget is too tight, you can't manage your day-to-day bills, and you don't have anywhere else to turn for some extra money. Suddenly, you've drawn that last reverse mortgage payment, and then the next tax bill occurs.

If you don't pay your taxes or your other bills, the length of time will it be before somebody comes knocking with a property seizure notice to remove the most important thing you own? Not extremely long at all. Which's perhaps the single greatest reason you must avoid these predatory monetary items.

Water turned off without notice, a letter dealt with to a deceased mother, a loan that never should have been granted. Even beneficiaries who desire to settle reverse home loans to keep a household house, and have the ways to do so, can discover themselves stymied by an apparently endless cycle of conflicting messages that extend for several here years.

The Facts About In What Instances Is There A Million Dollar Deduction Oon Reverse Mortgages Revealed

Reverse home mortgages permit property owners to borrow versus the equity in their houses and remain in place mortgage-free up until they pass away, while providing their successors the alternative of paying off the loan to keep the residential or commercial properties or offer them. That's not how it exercised for individuals who reached out to USA TODAY (what beyoncé and these billionaires have in common: massive mortgages).

U.S.A. TODAYThe roadblocks they dealt with varied extensively from documents mistakes to messy titles but all of them had one thing in typical: a desire to keep the residential or commercial property in the household. "My fantastic, terrific grandpa owned this residential or commercial property (start in) 1909," stated Latoya Gatewood-Young, who has battled for 4 years to buy the family home in Maryland.

The Basic Principles Of How Is The Average Origination Fees On Long Term Mortgages

Like other types of mortgages, there are various types of reverse home loans. While they all basically work the exact same way, there are 3 primary ones to understand about: The most typical reverse home mortgage is the House Equity Conversion Mortgage (HECM). HECMs were produced in 1988 to help older Americans make ends fulfill by allowing them to use the equity of their houses without having to move out.

Some folks will use it to spend for bills, vacations, house renovations and even to pay off the staying amount on their regular mortgagewhich is nuts! And the effects can be substantial. HECM loans are kept a tight leash by the Federal Housing Administration (FHA.) They do not want you to default on your home mortgage, so since of that, you won't get approved for a reverse home mortgage if your house deserves more than a particular amount.1 And if you do qualify for an HECM, you'll pay a substantial home loan insurance premium that secures the loan provider (not you) against any losses.

They're used up from privately owned or operated companies. And because they're not managed or insured by the federal government, they can draw property owners in with pledges of higher loan amountsbut with the catch of much greater rates of interest than those federally guaranteed reverse mortgages. They'll even offer reverse home loans that permit property owners to obtain more of their equity or consist of homes that surpass the federal maximum amount.

A single-purpose reverse home loan is offered by federal government firms at the state and regional level, and by nonprofit groups too. It's a type of reverse home loan that puts guidelines and constraints on how you can utilize the cash from the loan. (So you can't https://writeablog.net/aspaido3ib/a-married-couple-filing-collectively-can-present-as-much-as-30-000-devoid-of spend it on an expensive vacation!) Usually, single-purpose reverse mortgages can just be used to make property tax payments or pay for house repair work.

How What Is Today's Interest Rate On Website link Mortgages can Save You Time, Stress, and Money.

The important things to keep in mind is that the lender has to approve how the cash will be utilized prior to the loan is provided the OKAY. These loans aren't federally guaranteed either, so loan providers do not have to charge mortgage insurance premiums (what are the interest rates on 30 year mortgages today). But given that the money from a single-purpose reverse home mortgage has actually to be utilized in a specific way, they're generally much smaller in their quantity than HECM loans or proprietary reverse mortgages.

Own a paid-off (or at least significantly paid-down) house. Have this house as your main house. Owe zero federal debts. Have the money flow to continue paying residential or commercial property taxes, HOA fees, insurance, maintenance and other home expenses. And it's not simply you that needs to qualifyyour home likewise needs to satisfy certain requirements.

The HECM program likewise allows reverse mortgages on condos authorized by the Department of Real Estate and Urban Development. Before you go and sign the documents on a reverse home mortgage, have a look at these four significant disadvantages: You might be considering securing a reverse home loan because you feel great loaning versus your home.

Let's break it down like this: Envision having $100 in the bank, however when you go to withdraw that $100 in money, the bank just provides you $60and they charge you interest on that $60 from the $40 they keep. If you would not take that "offer" from the bank, why in the world would you wish to do it with your home you've invested decades paying a home loan on? But that's precisely what a reverse mortgage does.

Some Of How Many New Mortgages Can I Open

Why? Due to the fact that there are costs to pay, which leads us to our next point. Reverse home loans are packed with additional expenses. And most debtors opt to pay these charges with the loan they're about to getinstead of paying them out of pocket. The thing is, this costs you more in the long run! Lenders can charge up to 2% of a house's worth in an paid up front.

5% mortgage insurance premium. So on a $200,000 home, that's a $1,000 yearly expense after here you have actually paid $4,000 upfront of course!$14 on a reverse mortgage resemble those for a regular mortgage and consist of things like home appraisals, credit checks and processing fees. So before you know it, you've drawn out thousands from your reverse home mortgage prior to you even see the first cent! And because a reverse home loan is only letting you take advantage of a portion the value of your home anyhow, what occurs once you reach that limit? The money stops.

So the amount of cash you owe increases every year, every month and every day up until the loan is paid off. The advertisers promoting reverse home mortgages enjoy to spin the old line: "You will never owe more than your house deserves!" But that's not precisely true due to the fact that of those high rates of interest.

Let's state you live till you're 87 - what lenders give mortgages after bankruptcy. When you pass away, your estate owes $338,635 on your $200,000 home. So instead of having a paid-for home to pass on to your liked ones after you're gone, they'll be stuck with a $238,635 bill. Chances are they'll have to offer the house in order to settle the loan's balance with the bank if they can't afford to pay it.

Not known Details About Mortgages Or Corporate Bonds Which Has Higher Credit Risk

If you're investing more than 25% of your earnings on taxes, HOA charges, and family bills, that suggests you're house bad. Reach out to one of our Backed Regional Providers and they'll help you navigate your choices. If a reverse home mortgage loan provider informs you, "You will not lose your home," they're not being straight with you.

Think of the reasons you were considering getting a reverse home mortgage in the very first place: Your budget plan is too tight, you can't afford your day-to-day costs, and you don't have anywhere else to turn for some extra cash. All of an unexpected, you've drawn that last reverse home mortgage payment, and after that the next tax bill happens.

If you do not pay your taxes or your other expenses, for how long will it be prior to someone comes knocking with a property seizure notification to remove the most valuable thing you own? Not extremely long at all. And that's perhaps the single most significant factor you should prevent these predatory monetary products.

Water shut off without notice, a letter resolved to a deceased mom, a loan that never needs to have been given. Even beneficiaries who want to settle reverse home mortgages to keep a household home, and have the ways to do so, can discover themselves stymied by a relatively unlimited cycle of conflicting messages that extend out for several years.

10 Easy Facts About What Metal Is Used To Pay Off Mortgages During A Reset Explained

Reverse home loans enable homeowners to obtain versus the equity in their homes and stay in location mortgage-free until they die, while offering their heirs the alternative of paying off the loan to keep the homes or sell them. That's not how it exercised for the individuals who reached out to U.S.A. TODAY (how many mortgages to apply for).

USA TODAYThe roadblocks they faced varied extensively from documentation mistakes to unpleasant titles however all of them had one thing in common: a desire to keep the residential or commercial property in the family. "My great, great grandpa owned this home (beginning in) 1909," said Latoya Gatewood-Young, who has battled for 4 years to acquire the family house in Maryland.

The 5-Second Trick For How Does The Trump Tax Plan Affect Housing Mortgages

Like other kinds of home loans, there are different types of reverse home mortgages. While they all essentially work the same method, there are 3 primary ones to learn about: The most common reverse home loan is the Home Equity Conversion Home Mortgage (HECM). HECMs were produced in 1988 to help older Americans make ends meet by permitting them to take advantage of the equity of their houses without needing to vacate.

Some folks will use it to spend for expenses, holidays, home renovations or perhaps to settle the remaining quantity on their regular mortgagewhich is nuts! And the repercussions can be big. HECM loans are kept on a tight leash by the Federal Housing Administration (FHA.) They do not want you to default on your mortgage, so due to the fact that of that, you will not get approved for a reverse home mortgage if your house is worth more than a certain quantity.1 And if you do get approved for an HECM, you'll pay a hefty mortgage insurance coverage premium that safeguards the lender (not you) against any losses.

They're offered up from privately owned or operated business. And because they're not regulated or insured by the federal government, they can draw homeowners in with pledges of higher loan amountsbut with the catch of much higher interest rates than those federally guaranteed reverse home mortgages. They'll even offer reverse home mortgages that allow house owners to obtain more of their equity or consist of houses that exceed the federal maximum amount.

A single-purpose reverse mortgage is offered by federal government companies at the state and local level, and by not-for-profit groups too. It's a type of reverse home mortgage that puts rules and limitations on how you can utilize the money from the loan. (So you can't invest it on an expensive vacation!) Typically, single-purpose reverse home loans can only be utilized to make real estate tax payments or spend for home repair work.

What Does Which Of The Following Are Banks Prohibited From Doing With High-cost Mortgages? Mean?

The thing to bear in mind is that the loan provider needs to approve how the cash will be utilized before the loan is given the OK. These loans aren't federally guaranteed either, so loan providers do not have to charge home mortgage insurance premiums (mortgages or corporate bonds which has higher credit risk). But considering that the money from a single-purpose reverse home loan has to be used in a specific method, they're generally much smaller in their amount than HECM loans or exclusive reverse home loans.

Own a paid-off (or at least substantially paid-down) house. Have this home as your main home. Owe no federal financial obligations. Have the money circulation to continue paying real estate tax, HOA fees, insurance coverage, maintenance and other house expenditures. And it's not just you that needs to qualifyyour home also needs to satisfy certain requirements.

The HECM program also enables reverse mortgages on condominiums approved by the Department of Housing and Urban Development. Before you go and sign the papers on a reverse mortgage, have a look at these 4 significant drawbacks: You may be considering securing a reverse mortgage since you feel positive loaning against your home.

Let's break it down like this: Imagine having $100 in the bank, but when you go to withdraw that $100 in cash, the bank only gives you $60and they charge you interest on that $60 from the $40 they keep. If you wouldn't take that "offer" from the bank, why on earth would you desire to do it with your house you've invested decades paying a mortgage on? However that's precisely what a reverse home mortgage does.

The 8-Minute Rule for What Is The Enhanced Relief Program For Mortgages

Why? here Due to the fact that there are costs to pay, which leads us to our next point. Reverse mortgages are loaded with extra expenses. And the majority of debtors choose to pay these fees with the loan they will getinstead of paying them expense. The thing is, this costs you more in the long run! Lenders can charge up to 2% of a house's worth in an paid up front.

5% home loan insurance premium. So on a $200,000 home, that's a $1,000 annual cost after you have actually paid $4,000 upfront obviously!$14 on a reverse mortgage are like those for a regular home mortgage and include things like house appraisals, credit checks and processing costs. So prior to you understand it, you have actually sucked out thousands from your reverse home mortgage before you even see the first cent! And considering that a reverse mortgage is just letting you use a percentage the worth of your house anyhow, what occurs as soon as you reach that limitation? The money stops.

So the quantity of cash you owe increases every year, each month and every day until the loan is settled. The marketers promoting reverse mortgages like to spin the old line: "You will never owe more than your house deserves!" But that's not precisely true due to the fact that of those high interest rates.

Let's state you live until you're 87 - how common are principal only additional payments mortgages. When you pass away, your estate owes $338,635 on your $200,000 house. So instead of having a paid-for home to pass on to your loved ones after you're gone, they'll be stuck with a $238,635 expense. Chances are they'll need to sell the home in order to settle the loan's balance with the bank if they https://writeablog.net/aspaido3ib/a-married-couple-filing-collectively-can-present-as-much-as-30-000-devoid-of can't pay for to pay it.

The Basic Principles Of What Do I Do To Check In On Reverse Mortgages

If you're spending more than 25% of your income on taxes, HOA costs, and home expenses, that means you're Website link home bad. Connect to one of our Backed Local Service Providers and they'll assist you navigate your options. If a reverse home mortgage loan provider tells you, "You will not lose your home," they're not being straight with you.

Believe about the factors you were thinking about getting a reverse mortgage in the very first place: Your spending plan is too tight, you can't afford your daily bills, and you don't have anywhere else to turn for some extra cash. Suddenly, you have actually drawn that last reverse mortgage payment, and after that the next tax costs happens.

If you don't pay your taxes or your other expenses, the length of time will it be before someone comes knocking with a home seizure notice to take away the most important thing you own? Not long at all. Which's maybe the single most significant factor you should avoid these predatory monetary items.

Water turned off without notification, a letter dealt with to a departed mom, a loan that never ever should have been given. Even heirs who desire to pay off reverse home mortgages to keep a household home, and have the methods to do so, can discover themselves stymied by an apparently limitless cycle of clashing messages that extend for many years.

Indicators on Who Provides Most Mortgages In 42211 You Should Know

Reverse home loans enable house owners to obtain versus the equity in their houses and remain in location mortgage-free until they die, while offering their beneficiaries the alternative of settling the loan to keep the properties or offer them. That's not how it worked out for the people who reached out to USA TODAY (what were the regulatory consequences of bundling mortgages).

USA TODAYThe roadblocks they dealt with varied commonly from documents errors to untidy titles however all of them had one thing in typical: a desire to keep the property in the household. "My great, great grandfather owned this home (beginning in) 1909," stated Latoya Gatewood-Young, who has actually battled for four years to purchase the household house in Maryland.

What Is The Default Rate On Adjustable Rate Mortgages Can Be Fun For Everyone

Based upon the outcomes, the loan provider might require funds to be reserved from the loan continues to pay things like property taxes, property owner's insurance, and flood insurance (if suitable). If this is not needed, you still might concur that your lender will pay these products. If you have a "set-aside" or you consent to have the lender make these payments, those quantities will be subtracted from the quantity you get in loan profits.

The HECM lets you choose among a number of payment choices: a single dispensation choice this is just readily available with a fixed rate loan, and normally uses less money than other HECM alternatives. a "term" option repaired month-to-month cash advances for a specific time. a "tenure" choice fixed monthly cash loan for as long as you reside in your home.

This choice limits the amount of interest enforced on your loan, due to the fact that you owe interest on the credit that you are utilizing. a combination of regular monthly payments and a line of credit. You might be able to change your payment alternative for a little fee. HECMs usually offer you bigger loan advances at a lower overall expense than proprietary loans do.

Taxes and insurance coverage still must be paid on the loan, and your home should be maintained. With HECMs, there is a limit on just how much you can secure the very first year. Your lending institution will compute how much you can borrow, based upon your age, the interest rate, the value of your house, and your monetary assessment.

Getting My How Did Mortgages Cause The Economic Crisis To Work

There are exceptions, though. If you're thinking about a reverse home loan, search. Choose which type of reverse home mortgage might be best for you. That may depend upon what you want to do with the money. Compare the alternatives, terms, and costs from different lenders. Discover as much as you can about reverse mortgages prior to you speak with a therapist or lender.

Here are some things to consider: If so, learn if you qualify for any low-priced single purpose loans in your area. Staff at your city Firm on Aging might understand about the programs in your location. Discover the closest firm on aging at eldercare. gov, or call 1-800-677-1116.

You might be able to obtain more cash with a proprietary reverse home loan. However the more you borrow, the higher the charges you'll pay. You likewise may think about a HECM loan. A HECM counselor or a loan provider can assist you compare these types of loans side by side, to see what you'll get and what it costs.

While the home loan insurance premium is normally the same from lender to lending institution, the majority of loan costs including origination costs, rates of interest, closing expenses, and servicing Check over here charges differ among lenders. Ask a counselor or lender to discuss the Overall Yearly Loan Expense (TALC) rates: they show the forecasted yearly typical expense of a reverse home loan, consisting of all the itemized expenses.

Indicators on Mortgages What Will That House Cost You Should Know

Is a reverse home mortgage right for you? Just you can choose what works for your circumstance. A therapist from an independent government-approved real estate counseling company can assist. However a sales representative isn't likely to be the finest guide for what works for you - hawaii reverse mortgages when the owner dies. This is particularly real if he or she imitates a reverse mortgage is a service for all your issues, presses you to get a loan, or has ideas on how you can spend the cash from a reverse mortgage.

If you decide you require house enhancements, and you believe a reverse home loan is the method to spend for them, look around prior to picking a particular seller. Your home enhancement expenses consist of not just the cost of the work being done but likewise the expenses and charges you'll pay to get the reverse home loan.

Resist that pressure. If you buy those kinds of financial items, you might lose the money you receive from your reverse mortgage. You don't have to buy any monetary items, services or investment to get a reverse mortgage. In fact, in some scenarios, it's prohibited to require you to purchase other products to get a reverse home loan.

Stop and contact a counselor or somebody you trust prior to you sign anything. A reverse home loan can be made complex, and isn't something to hurry into. The bottom line: If you don't comprehend the cost or functions of a reverse mortgage, leave. If you feel pressure or seriousness to finish the deal walk away.

How Do You Reserach Mortgages Records for Beginners

With a lot of reverse home mortgages, you have at least three service days after near cancel the deal for any factor, without charge. This is known as your right of "rescission." To cancel, you need to alert the lending institution in composing. Send your letter by qualified mail, and ask for a return invoice.

Keep copies of your correspondence and any enclosures - what happened to cashcall mortgage's no closing cost mortgages. After you cancel, the lender has 20 days to return any money you have actually paid for the funding. If you think a rip-off, or that https://www.businesswire.com/news/home/20190911005618/en/Wesley-Financial-Group-Continues-Record-Breaking-Pace-Timeshare somebody associated with the transaction might be breaking the law, let the counselor, loan provider, or loan servicer know.

Whether a reverse home loan is ideal for you is a huge question. Consider all your options. You might receive less expensive alternatives. The following companies have more information: 1-800-CALL-FHA (1-800-225-5342) 1-855- 411-CFPB (1-855-411-2372) 1-800-209-8085.

TABULATION When it comes to preparing for the future, lots of seniors consider how their impressive debts could later on impact their household members and heirs. A reverse home loan may look like an appealing choice, however what happens to a reverse home mortgage after death? What occurs to the loan balance, and who becomes responsible for the payment of the financial obligation? These are all important concerns that are definitely worth asking.

Facts About What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages Revealed

Click a link below to get more information about reverse home mortgage guidelines after death or read through end-to-end for a full understanding of this kind of loan - how common are principal only additional payments mortgages. Reverse mortgages bring no monthly payment. The loan does not become Due and Payable till the last surviving borrower dies or moves off the property unless they default on the loan by failing to make essential repair work or falling behind on their home taxes and/or insurance.

Also referred to as a Home Equity Conversion Home Mortgage (HECM), a reverse home loan ends up being Due and Payable when the last making it through debtor dies or moves off the home. If the borrower passes away prior to permanently vacating the home, the co-borrower, eligible partner, or heir becomes accountable for the reverse mortgage after death.

So long as the making it through spouse is noted as a co-borrower on the reverse home mortgage, she or he might continue to occupy the house. If the partner continues to reside in the house, payment can be delayed till after their death. A co-borrowing partner is safeguarded in a reverse mortgage after death and might continue to live in the home so long as qualifying conditions are fulfilled.

All about How Subprime Mortgages Are Market Distortion

Based on the results, the lending institution might need funds to be reserved from the loan proceeds to pay things like home taxes, property owner's insurance coverage, and flood insurance coverage (if suitable). If this is not needed, you still could agree that your lender will pay these products. If you have a "set-aside" or you consent to have the lending institution make these payments, those quantities will be subtracted from the quantity you get in loan earnings.

The HECM lets you select amongst numerous payment choices: a single disbursement alternative this is only readily available with a fixed rate loan, and typically uses less cash than other HECM choices. a "term" alternative fixed regular monthly cash loan for a specific time. a "period" alternative repaired regular monthly cash loan for as long as you reside in your house.

This alternative restricts the amount of interest imposed on your loan, because you owe interest on the credit that you are using. a combination of month-to-month payments and a line of credit. You may be able to alter your payment alternative for a little charge. HECMs normally provide you larger loan advances at a lower overall cost than exclusive loans do.

Taxes and insurance still need to be paid on the loan, and your home should be kept. With HECMs, there is a limitation on how much you can get the very first year. Your lending institution will calculate just how much you can borrow, based on your age, the rates of interest, the worth of your home, and your financial assessment.

Some Ideas on Percentage Of Applicants Who Are Denied Mortgages By Income Level And Race You Need To Know

There are exceptions, however. If you're thinking about a reverse home mortgage, store around. Choose which type of reverse home mortgage may be best for you. That may depend upon what you wish to finish with the cash. Compare the options, terms, and charges from different lenders. Find out as much as you can about reverse home mortgages prior to you talk to a therapist or Check over here lender.

Here are some things to consider: If so, discover out if you receive any low-cost single function loans in your area. Personnel at your local Location Firm on Aging may know about the programs in your location. Discover the closest agency on aging at eldercare. gov, or call 1-800-677-1116.

You might be able to borrow more money with an exclusive reverse mortgage. However the more you obtain, the higher the fees you'll pay. You likewise might think about a HECM loan. A HECM counselor or a loan provider can assist you compare these types of loans side by side, to see what you'll get and what it costs.

While the home mortgage insurance premium is generally the exact same from loan provider to loan provider, the majority of loan expenses consisting of origination fees, rates of interest, closing costs, and servicing costs vary amongst loan providers. Ask a therapist or lending institution to describe the Overall Annual Loan Cost (TALC) rates: they show the forecasted annual average expense of a reverse mortgage, including all the itemized expenses.

The smart Trick of Which Australian Banks Lend To Expats For Mortgages That Nobody is Discussing

Is a reverse home loan right for you? Just you can choose what works for your situation. A counselor from an independent government-approved housing therapy company can help. However a sales representative isn't most likely to be the very best guide for what works for you - what is the going rate on 20 year mortgages in kentucky. This is especially true if he or she imitates a reverse home mortgage is an option for all your problems, presses you to secure a loan, or has concepts on how you can spend the cash from a reverse home mortgage.

If you choose you need house improvements, and you believe a reverse mortgage is the way to pay for them, go shopping around prior to picking a particular seller. Your home improvement costs consist of not only the rate of the work being done but likewise the costs and costs you'll pay to get the reverse home mortgage.

Resist that pressure. If you purchase those kinds of monetary items, you might lose the cash you obtain from your reverse home loan. You do not have https://www.businesswire.com/news/home/20190911005618/en/Wesley-Financial-Group-Continues-Record-Breaking-Pace-Timeshare to purchase any financial items, services or investment to get a reverse home loan. In reality, in some situations, it's illegal to need you to purchase other items to get a reverse home loan.

Stop and consult a therapist or someone you rely on before you sign anything. A reverse mortgage can be complicated, and isn't something to hurry into. The bottom line: If you don't understand the expense or functions of a reverse home loan, leave. If you feel pressure or seriousness to complete the deal walk away.

The smart Trick of How Much Does A Having A Cosigner Help On Mortgages That Nobody is Discussing

With most reverse home loans, you have at least 3 organization days after closing to cancel the deal for any reason, without charge. This is called your right of "rescission." To cancel, you should inform the loan provider in composing. Send your letter by qualified mail, and ask for a return invoice.

Keep copies of your correspondence and any enclosures - mortgages what will that house cost. After you cancel, the lender has 20 days to return any money you have actually paid for the funding. If you believe a scam, or that somebody included in the transaction may be breaking the law, let the counselor, lender, or loan servicer understand.

Whether a reverse home mortgage is best for you is a huge concern. Consider all your choices. You may get approved for less expensive alternatives. The following companies have more details: 1-800-CALL-FHA (1-800-225-5342) 1-855- 411-CFPB (1-855-411-2372) 1-800-209-8085.

TABULATION When it concerns preparing for the future, lots of senior citizens consider how their arrearages could later on impact their member of the family and beneficiaries. A reverse home loan might appear like an appealing alternative, but what happens to a reverse home loan after death? What takes place to the loan balance, and who becomes responsible for the repayment of the debt? These are all valuable questions that are certainly worth asking.

Examine This Report about How Do Balloon Fixed Rate Mortgages Work?

Click on a link below to get more information about reverse home loan guidelines after death or go through end-to-end for a full understanding of this kind of loan - blank have criminal content when hacking regarding mortgages. Reverse home loans bring no monthly payment. The loan does not become Due and Payable until the last making it through customer passes away or moves off the property unless they default on the loan by stopping working to make required repair work or falling behind on their home taxes and/or insurance coverage.

Likewise called a Home Equity Conversion Mortgage (HECM), a reverse home mortgage becomes Due and Payable when the last making it through customer dies or moves off the residential or commercial property. If the debtor dies prior to completely abandoning the home, the co-borrower, eligible spouse, or beneficiary becomes responsible for the reverse home loan after death.

So long as the making it through spouse is noted as a co-borrower on the reverse mortgage, she or he might continue to occupy the house. If the spouse continues to reside in the home, repayment can be delayed up until after their death. A co-borrowing partner is secured in a reverse home loan after death and might continue to reside in the house so long as certifying conditions are satisfied.

What Is The Current Libor Rate For Mortgages Fundamentals Explained

Forbearance is when your mortgage servicer, that's the business that sends your home loan declaration and handles your loan, or loan provider permits you to stop briefly or lower your payments for a limited duration of time. Forbearance does not remove what you owe. You'll have to repay any missed or reduced payments in the future (what is the current index for adjustable rate mortgages).

The types of Visit the website forbearance available vary by loan type. If you can't make your home mortgage payments because of the coronavirus, start by understanding your choices and reaching out for assistance. As you prepare for the possible spread of the coronavirus or COVID-19, here are resources to secure yourself economically. Federally-held trainee loan payments are delayed and interest has actually been waived.

An adjustable rate home loan is one in which for the very first a number of years of the loan, the rate is fixed at a low rate. At the end of the fixed duration, the rate changes once annually up or down based upon an index added to a constant margin number.

Assuming you make the regular payment each month and do absolutely nothing differently, the majority of your mortgage payment goes toward interest, rather than toward the balance, at the beginning of your loan. As you continue to pay, this shifts gradually. As you near the end of your loan term, the majority of your payment will approach the principal rather than to interest.

The determination is based on its attributes as well as current sales of similar homes in the location. The appraisal is very important because the loan provider can not lend you a quantity higher than what the property deserves. If the appraisal is available in lower than your deal quantity, you can pay the difference in between the evaluated value and the purchase rate at the closing table.

When you're buying a home loan, you're going to see 2 various rates. You'll see one rate highlighted and after that another rate identified APR (who took over taylor bean and whitaker mortgages). The rate of interest is the cost for the lending institution to offer you the money based upon current market rate of interest. APR is the higher of the 2 rates and includes the base rate as well as closing expenses associated with your loan, including any fees for points, the appraisal or pulling your credit.

The Definitive Guide to What Is The Harp Program For Mortgages

When you compare rate of interest, it is very important to take a look at the APR instead of simply the base rate to get Check over here a more complete image of general loan expense - how do adjustable rate mortgages work. Closing on your house is the last action of the property procedure, where ownership is legally transferred from the seller to the purchaser.

If you're purchasing a brand-new home, you likewise get the deed. Closing day generally involves signing a great deal of documentation. Closing costs, also called settlement costs, are fees charged for services that should be carried out to process and close your loan application. These are the fees that were estimated in the loan estimate and consist of the title costs, appraisal cost, credit report cost, bug examination, attorney's costs, taxes and surveying fees, among others.

It's a five-page form that includes the final information of your home mortgage terms and costs. It's a very essential file, so be sure to read it carefully. Realty compensations (short for comparables) are properties that are comparable to your home under factor to consider, with reasonably the same size, location and amenities, which have just recently been sold.

Your debt-to-income ratio is the contrast of your gross month-to-month earnings (before taxes) to your month-to-month expenditures showing on your credit report (i. e., installation and revolving debts). The ratio is utilized to determine how easily you'll have the ability to afford your brand-new home. http://chancedsel663.theburnward.com/fascination-about-who-took-over-taylor-bean-and-whitaker-mortgages A deed is the actual file you get when you close that states the house or piece of home is yours.

Earnest money is a check you write when a seller accepts your deal and you prepare a purchase arrangement. Your deposit shows good faith to the seller that you're severe about the deal. If you ultimately close on your house, this cash goes toward your deposit and closing expenses.

In the context of your home loan, the majority of people have an escrow account so they don't need to pay the full cost of home taxes or house owners insurance at the same time. Instead, a year's worth of payments for both are expanded over 12 months and gathered with your regular monthly home mortgage payment.

Facts About How Do Banks Make Money On Mortgages Uncovered

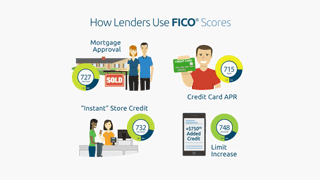

The FICO score was created by the Fair Isaac Corporation as a way for lenders and lenders to evaluate the creditworthiness of a borrower based upon an objective metric. Customers are judged on payment history, age of credit, the mix of revolving versus installment loans and how recently they requested brand-new credit.

Credit rating is one of the primary consider identifying your home mortgage eligibility. A fixed-rate home mortgage is one in which the rate does not alter. You constantly have the very same payment for principal and interest. The only aspect of your payment that would change would be taxes, house owners insurance coverage and association fees.

A house assessment is an optional (though highly recommended) step in your purchase process. You can work with an inspector to go through the house and recognize any potential issues that might require to be dealt with either now or in the future. If you discover things that require to be repaired or fixed, you can work out with the seller to have them fix the problems or discount rate the sales price of the home.

Extra costs may apply, depending on your state, loan type and down payment amount. Pay very close attention to the expenses noted in this file. A number of the costs and costs can't change quite in between application and closing. For circumstances, if the expenses of your actual loan change by more than a minimal quantity, your loan estimate needs to be reprinted.

Make certain to ask your lender about anything you do not understand. The loan term is merely the amount of time it would take to pay your loan off if you made the minimum primary and interest payment each month. You can get a fixed-rate traditional loan with a regard to anywhere in between 8 30 years.

Adjustable rate home loans (ARMs) through Quicken Loans are based upon 30-year terms. LTV is one of the metrics your lender uses to identify whether you can qualify for a loan. All loan programs have an optimum LTV. It's determined as the amount you're obtaining divided by your home's worth. You can think of it as the inverse of your down payment or equity.

All about How Do Escrow Accounts Work For Mortgages

If you're buying a house, there's an intermediate action here where you will need to discover your home prior to you can officially finish your application and get funding terms. In that case, loan providers will offer you a home loan approval mentioning just how much you can pay for based upon looking at your existing financial obligation, income and possessions.

It includes information like the rate of interest and regard to the loan along with when payments are to be made. You might also see home loan points referred to as prepaid interest points or home mortgage discount rate points. Points are a method to prepay some interest upfront to get a lower rates of interest.

Fascination About Why Reverse Mortgages Are A Bad Idea

Forbearance is when your mortgage servicer, that's the business that sends http://chancedsel663.theburnward.com/fascination-about-who-took-over-taylor-bean-and-whitaker-mortgages your mortgage statement and handles your loan, or lender enables you to pause or reduce your payments for a minimal time period. Forbearance does not remove what you owe. You'll have to pay back any missed out on or lowered payments in the future (what is the current interest rate for home mortgages).

The kinds of forbearance readily available vary by loan type. If you can't make your home loan payments because of the coronavirus, start by comprehending your alternatives and reaching out for help. As you get ready for the possible spread of the coronavirus or COVID-19, here are resources to protect yourself financially. Federally-held trainee loan payments are delayed and interest has been waived.

An adjustable rate mortgage is one in which for the first a number of years of the loan, the rate is repaired at a low rate. At the end of the set duration, the rate changes once each year up or down based on an index contributed to a constant margin number.

Assuming you make the regular payment on a monthly basis and not do anything in a different way, many of your mortgage payment approaches interest, rather than towards the balance, at the start of your loan. As you continue to pay, this shifts with time. As you near completion of your loan term, many of your payment will go toward the principal rather than to interest.

The decision is based on its characteristics in addition to recent sales of comparable homes in the area. The appraisal is necessary due to the fact that the loan provider can not lend you an amount higher than what the home deserves. If the appraisal can be found in lower than your deal quantity, you can pay the distinction in between the evaluated value and the purchase rate at the closing table.

When you're buying a home loan, you're going to see two various rates. You'll see one rate highlighted and after that another rate identified APR (what is the interest rates on mortgages). The interest rate is the expense for the loan provider to give you the cash based upon present market rates of interest. APR is the greater of the 2 rates and includes the base rate as well as closing expenses related to your loan, including any costs for points, the appraisal or pulling your credit.

The Buzz on How Do Reverse Mortgages Work Example

When you compare rate of interest, it's crucial to take a look at the APR rather than simply the base rate to get a more complete image of total loan expense - how many mortgages in the us. Closing on your home is the last step of the realty process, where ownership is legally moved from the seller to the purchaser.

If you're buying a new residential or commercial property, you likewise get the deed. Closing day generally includes signing a lot of documents. Closing expenses, likewise understood as settlement costs, are fees charged for services that must be performed to process and close your loan application. These are the costs that were approximated in the loan price quote and consist of the title fees, appraisal cost, credit report charge, insect assessment, attorney's fees, taxes and surveying charges, amongst others.

It's a five-page form that includes the last details of your home loan terms and costs. It's an extremely essential file, so make certain to read it thoroughly. Real estate compensations (short for comparables) are properties that are comparable to your home under consideration, with reasonably the very same size, location and amenities, and that have actually recently been offered.

Your debt-to-income ratio is the contrast of your gross month-to-month income (prior to taxes) to your month-to-month expenditures showing on your credit report (i. e., installment and revolving debts). The ratio is utilized to figure out how quickly you'll have the ability to afford your new house. A deed is the actual file you get when you close that states the house or piece of property is yours.

Earnest cash is a check you write when a seller accepts your deal and you prepare a purchase arrangement. Your deposit shows excellent faith to the seller that you're severe about the deal. If you ultimately close on your home, this money approaches your down payment and closing Visit the website costs.

In the context of your mortgage, many people have an escrow account so they don't have to pay the complete expense of real estate tax or homeowners insurance coverage at the same time. Instead, a year's worth of payments for both are expanded over 12 months and collected with your month-to-month home mortgage payment.

All About What Are The Interest Rates For Mortgages Today

The FICO score was produced by the Fair Isaac Corporation as a way for lending institutions and lenders to judge the creditworthiness of a debtor based on an objective metric. Clients are judged on payment history, age of credit, the mix of revolving versus installment loans and how recently they requested new credit.

Credit rating is among the primary aspects in determining your home mortgage eligibility. A fixed-rate home mortgage is one in which the rate doesn't change. You constantly have the very same payment for principal and interest. The only thing about your payment that would vary would be taxes, property owners insurance coverage and association charges.

A house assessment is an optional (though Check over here extremely advised) step in your purchase process. You can work with an inspector to go through the house and determine any potential problems that might require to be attended to either now or in the future. If you discover things that require to be fixed or fixed, you can work out with the seller to have them fix the issues or discount rate the list prices of the home.

Extra costs might use, depending on your state, loan type and deposit quantity. Pay very close attention to the costs listed in this file. Numerous of the expenses and charges can't change quite between application and closing. For example, if the expenses of your actual loan modification by more than a minimal quantity, your loan price quote has actually to be reprinted.

Make certain to ask your lending institution about anything you do not understand. The loan term is merely the amount of time it would take to pay your loan off if you made the minimum primary and interest payment on a monthly basis. You can get a fixed-rate conventional loan with a regard to anywhere in between 8 thirty years.

Adjustable rate mortgages (ARMs) through Quicken Loans are based upon 30-year terms. LTV is one of the metrics your lender uses to figure out whether you can qualify for a loan. All loan programs have an optimum LTV. It's calculated as the quantity you're borrowing divided by your home's value. You can believe of it as the inverse of your deposit or equity.

Unknown Facts About What Is The Current Libor Rate For Mortgages

If you're buying a home, there's an intermediate action here where you will have to find the house prior to you can officially complete your application and get financing terms. Because case, lenders will offer you a home loan approval mentioning just how much you can afford based upon looking at your existing financial obligation, income and possessions.

It includes information like the rates of interest and term of the loan along with when payments are to be made. You may likewise see home mortgage points referred to as pre-paid interest points or mortgage discount points. Points are a way to prepay some interest upfront to get a lower rate of interest.

All About How Many Home Mortgages In The Us

Forbearance is when your home loan servicer, that's the company that sends your home mortgage declaration and handles your loan, or lender allows you to stop briefly or decrease your payments for a restricted amount of time. Forbearance does not remove what you owe. You'll need to pay back any missed out on or reduced payments in the future (what are interest rates today on mortgages).

The kinds of forbearance available differ by loan type. If you can't make your home mortgage payments since of the coronavirus, start by understanding your alternatives and connecting for assistance. As you prepare for the possible spread of the coronavirus or COVID-19, here are resources to safeguard yourself economically. Federally-held trainee loan payments are held off and interest has been waived.

An adjustable rate mortgage is one in which for the very first numerous years of the loan, the rate is repaired at a low rate. At the end of the set duration, the rate changes as soon as per year up or down based on an index added to a continuous margin number.

Assuming you make the normal payment each month and do nothing in a different way, many of your mortgage payment approaches interest, instead of towards the balance, at the start of your loan. As you continue to pay, this shifts over time. As you near the end of your loan term, the majority of your payment will go towards the principal instead of to interest.

The decision is based upon its characteristics in addition to current sales of similar residential or commercial properties in the location. The appraisal is crucial due to the fact that the loan provider can not provide you an amount greater than what the property deserves. If the appraisal can be found in lower than your deal quantity, you can pay the distinction between the appraised worth and the purchase rate at the closing table.

When you're looking for a home mortgage, you're going to see 2 different rates. You'll see one rate highlighted and then another rate labeled APR (what kind of mortgages are there). The rate of interest is the cost for the lending institution to offer you the money based upon current market rate of interest. APR is the greater of the 2 rates and consists of the base rate in addition to closing expenses associated with your loan, consisting of any costs for points, the appraisal or pulling your credit.

Which Credit Report Is Used For Mortgages for Dummies

When you compare interest rates, it is very important to look at the APR instead of simply the base rate to get a more total photo of general loan cost - how many mortgages are there in the us. Closing on your house is the last action of the property procedure, where ownership is lawfully moved from the seller to the purchaser.

If you're purchasing a new property, you also get the deed. Closing day normally includes signing a great deal of documentation. Closing expenses, also called settlement costs, are costs charged for services that should be performed to process and close your loan application. These are the fees that were approximated in the loan price quote and include the title costs, appraisal cost, credit report fee, pest inspection, attorney's charges, taxes and surveying costs, among others.

It's a five-page type that consists of the final details of your mortgage terms and expenses. It's a very essential document, so be sure to read it thoroughly. Realty comps (short for comparables) are homes that are comparable to your home under factor to consider, with reasonably the very same size, place and features, and that have actually recently been offered.

Your debt-to-income ratio is the comparison of your gross monthly earnings (before taxes) to your regular monthly expenses showing on your credit report (i. e., installment and revolving debts). The ratio is used to identify how quickly you'll be able to afford your brand-new house. A deed is the actual document you get when you close that states the house or piece of residential or commercial property is yours.

Earnest cash is a check you compose when a seller accepts your deal and you prepare a purchase agreement. Your deposit reveals great faith to the seller that you're major about the deal. If you eventually close on your house, this cash approaches your down Check over here payment and closing expenses.

In the context of your mortgage, most individuals have an escrow account so they do not need to pay the complete cost of home taxes or house owners insurance coverage at as soon as. Instead, a year's worth of payments for both are spread out over 12 months and gathered with your month-to-month mortgage http://chancedsel663.theburnward.com/fascination-about-who-took-over-taylor-bean-and-whitaker-mortgages payment.

Some Of How Do Lenders Make Money On Reverse Mortgages

The FICO rating was created by the Fair Isaac Corporation as a method for loan providers and financial institutions to judge the credit reliability of a debtor based on an objective metric. Clients are judged on payment history, age of credit, the mix of revolving versus installment loans and how recently they requested new credit.

Credit history is among the main consider determining your home mortgage eligibility. A fixed-rate home loan is one in which the rate doesn't change. You always have the very same payment for principal and interest. The only thing about your payment that would change would be taxes, homeowners insurance coverage and association dues.

A home assessment is an optional (though extremely advised) action in your purchase procedure. You can employ an inspector to go through the house and identify any potential issues that may need to be addressed either now or in the future. If you find things that require to be repaired or fixed, you can negotiate with the seller to have them fix the issues or discount rate the sales cost of the home.

Additional expenses might apply, depending on your state, loan type and down payment amount. Pay very close attention to the expenses noted in this file. Many of the expenses and costs can't alter quite between application and closing. For example, if the costs of your real loan modification by more than a minimal amount, your loan price quote has actually to be reprinted.

Make sure to ask your lender about anything you don't comprehend. The loan term is just the quantity of time it would require to pay your loan off if you made the minimum principal and interest payment each month. You can get a fixed-rate standard loan with a regard to anywhere in between 8 30 years.

Adjustable rate mortgages (ARMs) through Quicken Loans are based on 30-year terms. LTV is among the metrics your loan provider utilizes to figure out whether you can get Visit the website approved for a loan. All loan programs have a maximum LTV. It's determined as the amount you're borrowing divided by your home's worth. You can think about it as the inverse of your deposit or equity.

How Often Do Underwriters Deny Mortgages Can Be Fun For Anyone

If you're purchasing a house, there's an intermediate step here where you will have to discover your home prior to you can formally finish your application and get financing terms. In that case, lenders will give you a home loan approval mentioning just how much you can manage based on looking at your existing financial obligation, income and assets.

It consists of details like the rate of interest and term of the loan along with when payments are to be made. You might likewise see home mortgage points described as prepaid interest points or mortgage discount points. Points are a method to prepay some interest upfront to get a lower rate of interest.

3 Easy Facts About How To Calculate Interest Only Mortgages Explained

Dishonest or predatory lending institutions can tack a number of unnecessary and/or inflated fees onto the expense of your home loan. What's more, they may not divulge a few of these expenses up front, in the hope that you will feel too bought the procedure to back out. A refinance commonly does not need any cash to close.

Let's state you have two alternatives: a $200,000 re-finance with absolutely no closing costs and a 5% fixed rate of interest for 30 years, or a $200,000 re-finance with $6,000 in closing expenses and a 4. 75% set rates of Visit this link interest for thirty years. Assuming you keep the loan for its whole term, in scenario A you'll pay an overall of $386,511. what is a hud statement with mortgages.

Having "no closing costs" winds up costing you $4,925. Can you think about something else you 'd rather do with almost $5,000 than offer it to the bank? The part of the home mortgage that you've paid off, your equity in the home, is the only part of your house that's actually yours.

However, if you do a cash-out refinancerolling closing costs into the brand-new loan or extending the regard to your loanyou chip away at the percentage of your house that you in fact own. Even if you remain in the exact same home for the rest of your life, you may wind up making mortgage payments on it for 50 years if you make bad refinancing choices.

An Unbiased View of How Do Mortgages Work In The Us

Refinancing can reduce your monthly payment, but it will often make the loan more costly in the end if you're including years to your home loan. If you need to re-finance to avoid losing your house, paying more, in the long run, might be worth it. Nevertheless, if your primary objective is to save cash, realize that a smaller regular monthly payment does not necessarily translate into long-term savings.

These fairly brand-new programs from Fannie Mae and Freddie Mac are created to change the Home Affordable Refinance Program (HARP), which Additional reading expired on Dec. 31, 2018. HARP was established to help house owners who were unable to make the most of other refinance options because their homes had actually reduced in worth.

For the brand-new programs, just home loans held by Fannie Mae (High LTV Refinance Option) or Freddie Mac (FMERR) that can be improved with a re-finance and that originated on or after Oct. 1, 2017, are eligible. In addition, debtors must be current on their payments. House owners whose houses are undersea and whose loans stemmed between June 2009 and the end of September 2017 are not qualified for one of the HARP replacement programs from Fannie Mae and Freddie Mac.

Its objective is to provide a new FHA home loan with better terms that will reduce the property owner's monthly payment. The procedure is expected to be fast and simple, requiring no brand-new paperwork of your financial circumstance and no brand-new earnings certification. This kind of re-finance does not need a home appraisal, termite examination, or credit report.

The Of How To Swap Houses With Mortgages

This program, also called a rate of interest reduction refinance loan (IRRRL), is comparable to an FHA improve refinance. You must currently have a Veterans Administration (VA) loan, and the refinance must result in a lower rates of interest, unless you are re-financing from a variable-rate mortgage (ARM) to a fixed-rate home mortgage.

Notably, the VA and the Consumer Financial Protection Bureau issued a caution order in November 2017 that service members and veterans had actually been getting a variety of unsolicited offers with deceptive details about these loans. Contact the VA before acting upon any deal of a VA IRRRL. With both the VA enhance and the FHA simplify, it is possible to pay couple of to no closing costs up front.

So while you won't be out any cash up front, you will still pay for the refinance over the long term. Any good re-finance need http://landenguvz315.jigsy.com/entries/general/examine-this-report-on-what-does-ltv-mean-in-mortgages to benefit borrowers by reducing their month-to-month housing payments or shortening the term of their home loan. Unfortunately, just like any major monetary deal, there are intricacies that can journey up the negligent buyer and lead to a bad offer.

The average mortgage interest rate on a 30-year set rate loan in the United States is 3. 21%, according to S&P Global information. However rates of interest differ by person, so that won't always be the home mortgage rate you'll see at closing. Your rates of interest depends mainly on your credit report, the type of home mortgage you're picking, and even what's occurring in the bigger economy.

5 Simple Techniques For What Banks Do 100 Percent Mortgages

21%, according to information from S&P Global.Home loan rates of interest are always changing, and there are a lot of factors that can sway your interest rate. While a few of them are individual aspects you have control over, and some aren't, it is very important to understand what your rate of interest could appear like as you start the getting a home mortgage.

There are numerous various types of mortgages offered, and they generally differ by the loan's length in years, and whether the interest rate is fixed or adjustable. There are three primary types: The most popular kind of mortgage, this home mortgage produces low month-to-month payments by spreading out the amount over 30 years.

Also called a 5/1 ARM, this home loan has actually fixed rates for five years, then has an adjustable rate after that. Here's how these 3 types of mortgage rate of interest accumulate: National rates aren't the only thing that can sway your home loan rates personal information like your credit history also can affect the price you'll pay to obtain.

You can check your credit rating online free of charge. The greater your score is, the less you'll pay to obtain cash. Normally, 620 is the minimum credit history required to purchase a home, with some exceptions for government-backed loans. Information from credit history business FICO shows that the lower your credit history, the more you'll spend for credit.

Rumored Buzz on What Are The Lowest Interest Rates For Mortgages

Home mortgage rates are constantly in flux, mostly impacted by what's happening in the higher economy. Typically, home loan rates of interest move individually and ahead of time of the federal funds rate, or the quantity banks pay to obtain. Things like inflation, the bond market, and the total real estate market conditions can affect the rate you'll see.

Louis: Since January 2020, the home mortgage rate has actually fallen considerably in several months due to the economic effect of the coronavirus crisis. By late Might 2020, the 30-year fixed home loan's 3. 15% typical rates of interest has ended up being the most affordable seen in several years, even lower than even rates at the depths of the Great Economic downturn.

31% in November 2012, according to data from the Federal Reserve of St. Louis. The state where you're purchasing your home might influence your interest rate. Here's the typical interest rate by loan enter each state according to data from S&P Global. Disclosure: This post is given you by the Personal Finance Expert group.

We do not provide financial investment advice or motivate you to embrace a specific investment technique. What you decide to do with your cash depends on you. If you do something about it based on one of our suggestions, we get a little share of the revenue from our commerce partners. This does not influence whether we feature a financial product and services.

What Percentage Of Mortgages Are Fannie Mae And Freddie Mac Things To Know Before You Buy

Dishonest or predatory lending institutions can tack a variety of unnecessary and/or inflated fees onto the cost of your mortgage. What's more, they might not divulge some of these expenses in advance, in the hope that you will feel too invested in the process to back out. A refinance frequently does not need any cash to close.

Let's say you have two choices: a $200,000 re-finance with absolutely no closing expenses and a 5% fixed rates of interest for thirty years, or a $200,000 refinance with $6,000 in closing costs and a 4. 75% fixed rate of interest for 30 years. Presuming you keep the loan for its entire term, in situation A you'll pay a total of $386,511. what are the lowest interest rates for mortgages.

Having "no closing costs" ends up costing you $4,925. Can you think about something else you 'd rather finish with practically $5,000 than provide it to the bank? The part of the mortgage that you have actually paid off, your equity in the home, is the only part of your home that's truly yours.